AI SaaS companies are valued at a median 25.8x revenue, significantly higher than non-AI SaaS companies, which typically trade at 5x–8x revenue. Why? Investors see AI as a game-changer due to faster growth (63% higher than non-AI SaaS), proprietary technology, and deep integration into workflows. Companies like Anthropic and Databricks showcase this trend, achieving valuations of $183 billion and $134 billion, respectively, with revenue multiples exceeding 27x.

Key insights:

- AI SaaS Growth: AI companies reach $100M ARR in 18–36 months, far faster than non-AI SaaS.

- Valuation Drivers: Proprietary data, high gross margins (75%+), and workflow lock-in boost multiples by 0.5x–2x ARR.

- Investor Focus: Metrics like Net Revenue Retention (120%+), compute cost efficiency, and revenue predictability now matter more than hype.

For SaaS founders, integrating AI effectively, improving core financial metrics, and showcasing tangible ROI can significantly increase valuations.

What Drives 25.8x Revenue Multiples for AI SaaS

Market Demand and Growth Potential

The way investors evaluate AI SaaS companies has shifted. It's no longer enough to showcase "AI potential" - they want tangible results. Metrics like time saved, revenue growth, and improved productivity are now the benchmarks for investment. In fact, organizations using AI tools report productivity gains of 50%–70% [1][7][2].

The numbers back up this demand. AI software companies are on track to grow 63% faster in 2024 than traditional software firms, driven by intense customer interest [2]. This momentum is reflected in venture capital trends: AI companies captured $89.4 billion in funding, roughly one-third of all VC dollars. By mid-2025, AI startups accounted for 53% of global VC funding [4].

The market has also begun to differentiate. "Category-Defining SaaS" companies - those offering groundbreaking solutions - command high revenue multiples, while "Commodity SaaS" with basic AI integrations often trades at 5x or less [8]. Even at early funding stages, AI startups are raising capital at valuations 40% higher than their non-AI counterparts, especially in data-intensive industries like fintech, logistics, and legal tech [3][7].

This growth and investor confidence underscore one key point: AI technology itself is becoming the ultimate differentiator.

AI Technology as a Competitive Edge

AI's ability to create defensible advantages lies in its use of proprietary datasets and feedback loops, which improve accuracy and make switching providers more difficult over time [1]. The real game-changer is "workflow ownership" - where AI doesn’t just enhance tasks but integrates deeply with business outcomes [1][12].

This technical edge directly impacts valuations. AI-native products with unique datasets and gross margins above 75% can achieve revenue multiples 2–3 times higher than traditional SaaS [1]. For example, "AI Supernovas" boast an average of $1.13 million in Annual Recurring Revenue (ARR) per full-time employee - 4–5 times higher than typical SaaS companies [10].

Valuation premiums also vary by the type of AI solution. Companies like OpenAI and Anthropic, categorized as "Strategic Anchors", can exceed 60x revenue multiples, while data and analytics agents average around 32.5x [9]. The market rewards firms that evolve from "Systems of Record" (data storage) to "Systems of Action" (automating workflows and executing tasks) [10].

While technology creates these advantages, financial discipline ultimately validates them.

Financial Metrics That Matter

Investors have shifted their focus. Instead of prioritizing rapid growth at any cost, they now value predictable, repeatable revenue streams - what some call "underwritable performance" [12]. In this context, the quality of revenue takes precedence over its sheer size.

"Investors are pricing the quality of the revenue, not the excitement of the category."

- Lior Ronen, Finro Financial Consulting [12]

Margin stability is another key factor. AI companies must show that infrastructure and compute costs - like API tokens and GPU expenses - decrease as a percentage of revenue over time [1][12]. To stand out, AI SaaS firms typically need Net Revenue Retention (NRR) above 120%, proving their ability to grow revenue from existing customers [1]. Interestingly, the focus has shifted from customer acquisition costs (CAC) to compute costs. As Talia Goldberg of Bessemer Venture Partners notes:

"COGS (cost of goods sold) is the new CAC. In SaaS, the constraint was customer acquisition cost. In AI, the constraint is compute cost."

- Talia Goldberg, Partner, Bessemer Venture Partners [11]

Recent examples highlight these principles in action. In January 2026, the AI-native search platform Glean achieved a $7.2 billion valuation with $200 million ARR, translating to a 36.0x revenue multiple [9]. Similarly, Hebbia earned a 53.8x multiple with a $700 million valuation on just $13 million in revenue, thanks to its focus on high-value data analytics [9]. Meanwhile, Cognigy was acquired for $955 million on $37 million in revenue, reflecting a 25.8x multiple driven by its enterprise-level repeatability [9].

Part 2: How To Sell Your Business At The Highest Valuation Multiple | Dirk Sahlmer, saas.group

AI SaaS vs. Traditional SaaS: Valuation Comparison

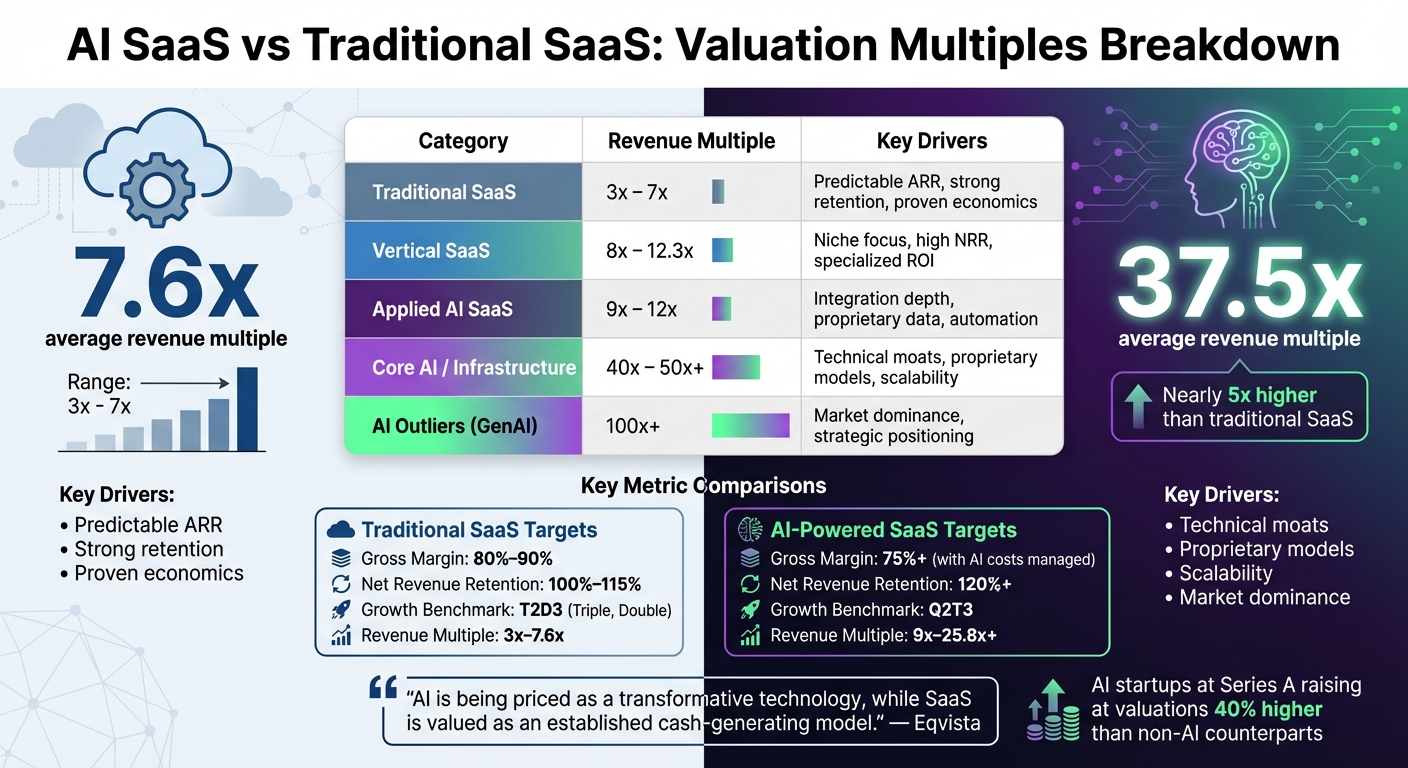

AI SaaS vs Traditional SaaS Valuation Multiples Comparison

Revenue Multiple Differences

AI startups are seeing revenue multiples that average 37.5x, compared to just 7.6x for traditional SaaS companies - a nearly fivefold difference[3]. Public AI companies also trade at higher multiples, often exceeding 10x revenue, while traditional SaaS businesses hover below 5x revenue[3].

"AI is being priced as a transformative technology, while SaaS is valued as an established cash-generating model."

The type of AI makes a big difference. Companies working on core AI - such as infrastructure and foundational models - fetch the highest premiums, with large language model (LLM) vendors averaging 44.1x revenue multiples[15]. On the other hand, Applied AI companies, which focus on specific functions like marketing or HR, trade between 9x and 12x. Meanwhile, Vertical SaaS platforms, which solve industry-specific challenges, typically see multiples around 12.3x[3][5][12].

These multiples highlight how factors like market positioning, niche specialization, and technical advantages influence valuation.

| Category | Typical Revenue Multiple | Key Drivers |

|---|---|---|

| Traditional SaaS | 3x – 7x | Predictable ARR, strong retention, proven economics |

| Vertical SaaS | 8x – 12.3x | Niche focus, high NRR, specialized ROI |

| Applied AI SaaS | 9x – 12x | Integration depth, proprietary data, automation |

| Core AI / Infrastructure | 40x – 50x+ | Technical moats, proprietary models, scalability |

| AI Outliers (GenAI) | 100x+ | Market dominance, strategic positioning |

Investors are increasingly favoring businesses with strong fundamentals and clear revenue streams, which explains the premium multiples for companies that can demonstrate consistent performance[12].

Regional and Industry Variations

Valuations also vary based on location and industry. North American AI startups tend to command higher multiples, thanks to robust venture capital ecosystems and proximity to major tech buyers. For example, AI startups at the Series A stage are raising at valuations 40% higher than their non-AI counterparts[3].

Industry-specific AI tools, often called Vertical AI, are following a path similar to traditional SaaS in the 2010s. Solutions in areas like legal tech, fintech, healthcare, and logistics are earning higher valuations due to their ability to tackle high-value, niche problems. These tools benefit from limited competition in their specialized markets[7].

The funding landscape reflects this trend. In the first half of 2025, AI startups captured 53% of global venture capital funding[4]. Median pre-money valuations show a steady climb across stages:

- $10 million for seed rounds

- $45.7 million for Series A

- $366.5 million for Series B

- $795.2 million for Series C[14]

Capital efficiency is becoming a key differentiator. Investors are closely watching EV/Funding ratios to identify companies that deliver value without excessive spending. Applied AI companies with strong distribution networks and clear customer renewal paths tend to earn higher multiples, especially when they move beyond experimental phases[12].

Real AI SaaS Exit Examples

Recent high-profile exits illustrate these valuation trends. In October 2025, OpenAI completed a secondary share sale at a staggering $500 billion valuation, based on projected 2025 revenue of $3 billion - equating to a 167x revenue multiple[16][17]. Major investors in this deal included Microsoft, Nvidia, SoftBank, and Thrive Capital.

"OpenAI's valuation defies traditional SaaS metrics."

- Matthew Barbieri, Partner, Wiss[16]

Similarly, in November 2025, Elon Musk's xAI was reportedly raising $15 billion at a $230 billion valuation, yielding an eye-popping 330x EV/Revenue multiple, reflecting its infrastructure-heavy focus[16][5].

Not every AI exit reaches such astronomical levels. For instance, in November 2024, hospitality software firm Mews acquired Atomize, an AI-powered revenue management platform, for approximately SEK 500 million (around $45 million)[17]. Other examples include Magic and Tabs, which traded at revenue multiples of 153x and 195x, respectively, though both struggled with lower capital efficiency compared to their funding levels.

"Investors are pricing the quality of the revenue, not the excitement of the category."

- Lior Ronen, Founder, Finro Financial Consulting[12]

For founders, the key takeaway is that while AI companies enjoy higher valuations, long-term success depends on building repeatable revenue streams, maintaining strong demand, and demonstrating solid unit economics - not just riding the AI hype[12].

sbb-itb-9cd970b

How to Increase Your SaaS Valuation

Improve Your Core Metrics

In today’s market, investors expect more than just promises - they want measurable results, especially when it comes to AI. To avoid valuation discounts, you need to show clear evidence that your AI features deliver tangible benefits like improved accuracy, time savings, or revenue growth. For instance, keeping gross margins above 75% and achieving a Net Revenue Retention (NRR) of over 120% can significantly boost your valuation[1]. Be cautious about relying too heavily on third-party APIs, as this can lead to 0.5x–1x ARR discounts[1].

Efficiency is another key factor. The EV/Funding ratio helps identify companies that use capital effectively. A great example is GoCharlie, which achieved over 100x EV/Funding and a 35x EV/Revenue multiple, proving how efficiency can drive higher valuations[5].

Revenue predictability also matters. Buyers value contracted, repeatable revenue tied to specific workflows over less predictable usage-based models. For example, a micro-SaaS company with $500,000 ARR optimized its support automation tool by reducing token spend by 22% through intent-based routing and fine-tuning. By introducing a premium tier, they boosted gross margins from 58% to 70% and sold at a 3.5x ARR multiple instead of 2.8x[1].

Once your financial metrics are solid, the next step is integrating AI to set your product apart.

Add AI to Your Product

After strengthening your core metrics, incorporating AI into your product can drive even higher valuations. Done right, AI can add a 0.5x–2x ARR multiple if you show that your product benefits from proprietary data or workflow lock-in[1]. However, the quality of your AI matters more than the hype. Products where AI is deeply integrated and tied to outcomes fetch higher premiums than those with superficial or "cosmetic" AI features[1].

"AI valuation premiums accrue to products where intelligence is inseparable from outcomes and protected by proprietary data... not to cosmetic AI features."

- Amanda White, SaaS Valuation Resources[1]

Take Cursor, an AI code editor, as an example. They developed a proprietary model that runs 4x faster than frontier models, enabling them to surpass $1 billion in annualized revenue while projecting gross margin improvements from 74% to 85% by 2027[18]. Optimizing architecture with model routing and caching is crucial for maintaining margins at scale[1][18].

To make your AI features indispensable, embed them into your customers' core workflows. Use proprietary datasets and feedback loops to demonstrate measurable improvements in accuracy or increased switching costs. Bundle these features into premium tiers with usage limits to protect margins while showcasing their value[1]. Also, ensure you maintain clear, auditable data lineage - vague data rights can lead to 25% valuation discounts or costly legal issues, as Anthropic discovered with their $1.5 billion settlement in 2025 over unauthorized training data[18].

Prepare for Growth and Exit

With strong metrics and AI integration, strategic growth and exit planning can further enhance your SaaS valuation. The growth benchmark for AI startups has shifted from the traditional "T2D3" model (triple, triple, double, double, double) to "Q2T3" (quadruple, quadruple, triple, triple, triple)[10]. Top-performing AI and SaaS companies are growing at an average of 65.4%, compared to the median growth rate of 28.3%[6]. To meet these benchmarks, prepare a comprehensive diligence package covering model architecture, data lineage, privacy controls, and cost-per-outcome metrics[1].

If you’re planning an exit that involves European markets, compliance with the EU AI Act is critical. This regulation, fully applicable as of August 2, 2026, imposes fines of up to €35 million or 7% of turnover for non-compliance[18]. For autonomous AI systems, establish robust oversight frameworks to mitigate "Autonomy Risk" and avoid valuation penalties[18].

Strategic acquisitions can also help boost your valuation. Acquiring AI-focused teams can fill capability gaps and transform a traditional SaaS asset (valued at 3x–5x multiples) into an AI-enhanced asset with mid-teens multiples[19]. Align funding rounds or exit plans with major product launches or technical milestones to maximize your perceived value[4].

| Metric | Traditional SaaS | AI-Powered SaaS Target |

|---|---|---|

| Gross Margin | 80%–90% | 75%+ (with AI costs managed) |

| Net Revenue Retention | 100%–115% | 120%+ |

| Growth Benchmark | T2D3 | Q2T3 |

| Revenue Multiple | 3x–7.6x | 9x–25.8x+ |

Conclusion: Maximize Your SaaS Valuation

The difference between traditional SaaS valuations at 7.6x revenue and AI SaaS at 25.8x isn't just a matter of technology - it's about proving substance over hype. The market now prioritizes software reliability and measurable business impact over lofty "autonomy" claims[9][12]. To boost your valuation, focus on strengthening your core metrics, strategically incorporating AI, and being prepared for detailed technical evaluations.

One key area to emphasize is building data moats that create genuine switching costs. Products where AI is deeply embedded into workflows and supported by proprietary feedback loops can add 0.5x–2x ARR to valuations. On the flip side, shallow AI features tend to bring in much smaller premiums[1][18]. Make sure to document your data lineage carefully - missteps in data rights management can lead to significant legal risks, potentially wiping out valuation gains[18].

"Valuation has shifted from 'how intelligent is the agent?' to 'how reliably does it behave as software?'"

- Lior Ronen, Founder, Finro Financial Consulting[9]

To position yourself for better funding rounds or strategic exits, focus on scalable technology execution. Traditional SaaS companies often achieve 80%–90% gross margins, but AI-native products frequently see margins drop to 50%–60% due to inference costs[18]. Use methods like model routing and caching to show that your margins can improve as you scale. This reinforces the importance of demonstrating ROI and efficient cost management, now critical metrics for investors. Track and report your cost-per-outcome, as investors increasingly scrutinize this during diligence[1].

When planning your next funding round or exit, align it with major technical milestones to justify higher multiples[4]. Whether you're aiming for 9x–12x for vertical AI or 20x+ for platform infrastructure, the companies securing premium valuations are those delivering measurable ROI today - not just promising it for the future[5][13].

FAQs

Is my SaaS really “AI” enough to earn a higher multiple?

Your SaaS can achieve a higher valuation multiple by focusing on delivering AI-driven outcomes that matter, utilizing proprietary data, and building strong, defensible AI capabilities. Simply adding surface-level AI features won’t cut it - investors are looking for products where AI plays a central role in driving results. Alongside this, factors like growth rate and market positioning carry weight. To secure premium valuations, it’s crucial to demonstrate how your AI directly impacts outcomes.

Which metrics move AI SaaS valuations the most?

Key elements that impact the valuation of AI SaaS companies include proprietary technology, data assets, defensibility, and market demand. Solutions that deliver measurable outcomes through advanced intelligence - especially when backed by exclusive data or self-reinforcing feedback loops - tend to attract higher valuations.

Revenue multiples, which can surpass 25–30×, are influenced by factors like control over core models and infrastructure, specialization in a specific market, efficient use of capital, and the ability to maintain a competitive edge through model defensibility.

How do I reduce AI compute costs without hurting growth?

To keep AI compute costs in check while still supporting growth, the key is efficiency and smart optimization. This means fine-tuning token usage, upgrading infrastructure, and making models work more effectively. For instance, OpenAI has managed to boost compute margins by refining their infrastructure and streamlining processes. By conducting thorough technical reviews, you can pinpoint areas to cut down on unnecessary token usage and ensure your AI models run cost-effectively without compromising their ability to drive growth.

Related Blog Posts

- From Hype to High-Value Exits: AI's Role in Private Equity's Future

- How to Command Premium Valuations in SaaS: Lessons from AI-First Companies

- The SaaS Valuation Gap: Why Typical Firms Stall at 4-6× While AI-Enabled Ones Hit 10×+

- The Future of SaaS Valuations: What the Best Companies Are Doing Differently